Content

QuickBooks is the finest tool for online banking and reconciliation. The balance sheets of a company contain its assets, liabilities, and equity. This sheet is balanced only when the assets are equal to the sum of liabilities and equity. In QuickBooks, these are mentioned under the reconciliation documents. Here assets are owned by the company, liabilities are what the company owes to a third party and equity is the amount of money that retains as a profit.

Enterprise Accounting Software Market (Latest Report CAGR) 2023 … – Digital Journal

Enterprise Accounting Software Market (Latest Report CAGR) 2023 ….

Posted: Sun, 05 Feb 2023 08:00:00 GMT [source]

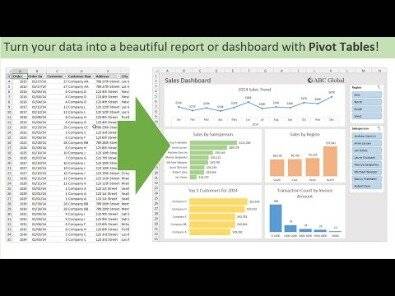

Open any report, click on “Excel” button and then create new worksheet. A P&L or Income Statement is a business report showing Net Income as the difference between Revenue and Expenses. Inventory assemblies are the ability to take individual items in the Item List and create them into a unique Item in that list. Let’s say, for example, that you operate a gift shop and wish to create a gift basket with individual items in your Item List. You have chocolate hearts, chocolate flowers, stickers, mugs, and caramel popcorn that you want to include in the basket, as well as the basket itself. In QB you can take each of these individual items and combine them into a brand-new item in the Item List.

What are liabilities in accounting?

Someone who is hoping to focus their future on the accounting field will be more likely to excel on your team. In accounting, it’s easy to miss a step, number, or other apparent detail. Left undetected, errors like this can have serious implications, ranging from uncollected receivables, duplicate payables, tax liability resulting in penalties and interest, and more.

Learn how to manage the finances for your small business yourself accounting package. Establishment of QuickBooks account is over, learn how to create an estimate and purchase order, send an invoice, receive payment and point check. The bank reconciliation for a company’s checking account begins with the company noting the balance per the bank statement and then making some notations about that balance. For example, the balance on the bank statement is probably not the amount that appears in the company’s records.

QuickBooks Interview Questions for Freshers:

This Top Quickbooks Interview Questionss that all financial transactions are correctly recorded and accounted for. Employers and hiring managers are looking for someone with strong accounting skills. Be prepared to explain the specifics of your experience and any technical specialty areas you have expertise in, such as tax preparation or bookkeeping. Top 7 accountant interview questions with detailed tips for both hiring managers and candidates. While being clear and concise, delve deeper into your job profile and make the recruiter construe the process. Try to include the accounts, financial statements, and whatever else you were responsible for.

When a user cancels a QuickBooks Online subscription, Intuit keeps the data for one year. Prior to canceling, you should export and/or print any necessary reports. You could even consider converting the data to a QuickBooks Desktop version for further accessibility. If you reinstate your account within a year after canceling it, QuickBooks will still have your historical data. Find answers to some of the most common QuickBooks questions from users, plus resources for more information.

Explain what happens if you don’t pay the estimated tax or miss the tax payment?

Dress to impress – Make sure to dress professionally and present yourself well when attending a job interview as an accountant. A polished look can make a positive impression on potential employers and increase your chances of landing the job. Understanding what qualities and qualifications are valued most in an employee can help determine if you have all of the necessary skills for the job or if areas need improvement. Additionally, it can give you insight into the company’s goals and values. I also use my knowledge of accounting principles and standards, such as Generally Accepted Accounting Principles , to ensure data consistency and accuracy.

- Also, QuickBooks can be used for making tax files, accounting reports and send an invoice to customers.

- I began by going through both sets of data line-by-line and comparing them against each other.

- In accounting, it’s easy to miss a step, number, or other apparent detail.

- Your answer should assure the hiring managers that you have the skills and training to fulfill the role’s duties and exceed expectations.

- It will also give you an idea of the resources available for ongoing development.

He was named Top 100 ProAdvisor by Insightful Accountant in 2014, 2015 and 2016, and Top 40 under 40 by CPA Practice Magazine in 2015. In addition, he is the co-host of QB Power Hour and host of ENTERPRISE.expert. In QuickBooks the term hosting or QuickBooks cloud refers to the QuickBooks data that is stored on a web server. This web server belongs to the enterprise or the company that is protected and maintained by the firm only. It is like having QuickBooks data that can be accessed only by the secured members of the company through an intranet.

Explain how to produce reoccurring invoices in Quickbooks?

The goal of your response is to provide evidence that you bring integrity to the workplace and that you are unafraid to have uncomfortable conversations. Since the HireVue interview is likely your first introduction to Intuit, you can give a high-level overview of your salary expectations. The hiring managers at Intuit would like an idea of what a competitive job offer looks like to you. The goal of your response is to describe the compensation plan you’re looking for while supporting your salary request with research and facts. The hiring managers at Intuit would like to know what captures your interest outside the workplace.

Specify the number to be notified for the overdue invoices before they reach their given due date. Click import and the expenses will be automatically added to the QuickBooks.

The accounting cycle is a collective process of identifying, analyzing, and recording the accounting events of a company. It is a standard 8-step process that begins when a transaction occurs and ends with its inclusion in the financial statements. Financial accounting is a branch of accounting involving in a process of recording, summarizing, and reporting financial transactions resulting from business operations over some time. Accounting is the process of recording, classifying, and summarizing financial transactions to provide information that is useful in making business decisions. It is an important tool for managers and business owners, as it can help them make informed decisions about how to allocate their resources.

- Accounting involves the collection, organization, recording, summarizing, and reporting of financial transactions for a company.

- Once you know the company/department’s primary needs, you can frame a precise answer to this question.

- Explain how the change directly impacted your job and talk about how you maintained a positive approach during the transition.

- Computerized accounting refers to carrying out accounting functions or processes using computers.

- I have maintained its prominence by continuing with the CPE annual requisite by attending training and workshops.

For instance, if time management is a weakness, the interviewer might wonder if you can meet your deadlines or if you are frequently late to work. For this reason, it’s best to choose weaknesses that will not impact your ability to succeed in the role. The hiring managers at Intuit are looking for evidence that you know your shortcomings. They also want to see that you embrace opportunities to grow and improve. The goal of your response is to show the decision-makers that you are self-aware, reflective, and can readily identify areas for improvement. Keeping an opportunity mindset, you can see why providing an opportunity-related response is the most effective approach.